Table of Contents

- Key Factors in Evaluating Tax Legislation

- How Proposed Tax Legislation is Assessed

- Baselines

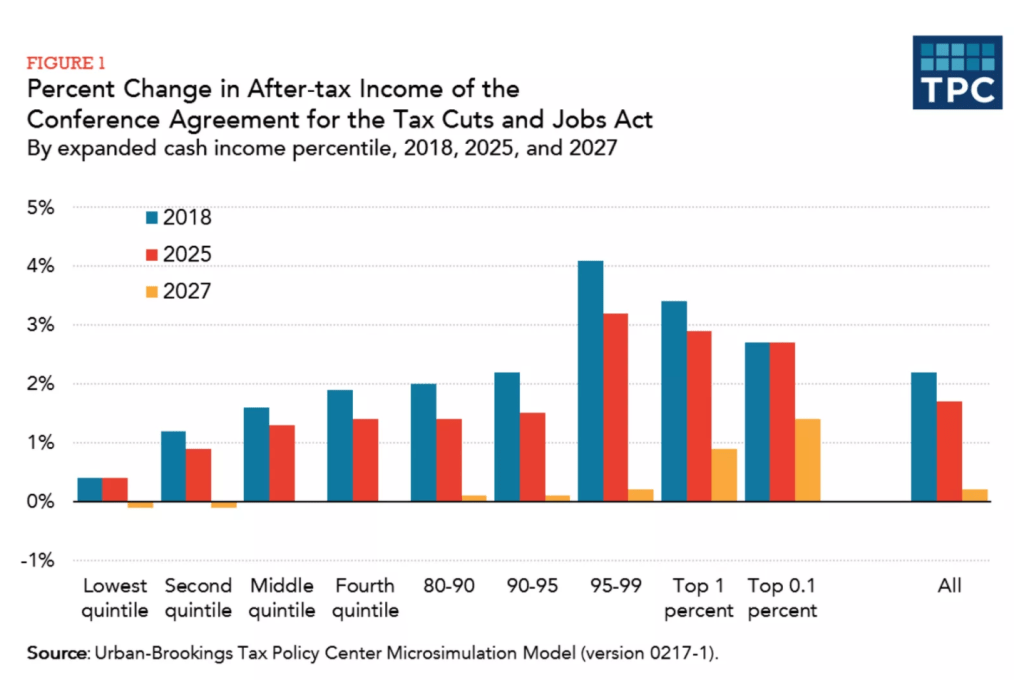

- Percent Change in After-tax Income

- Addenda

Key Factors in Evaluating Tax Legislation

- Using the right baseline.

- Using percent change in after-tax income to assess the effect on individual taxpayers

How Proposed Tax Legislation is Assessed

- Congressional Budget Office generates baseline projection

- cbo.gov/about/processes#methodology

- Baseline projections reflect CBO’s best judgment about how the economy and the budget will evolve under existing laws. That approach allows the baseline to serve as a neutral benchmark against which Members of Congress can measure the effects of proposed legislation.

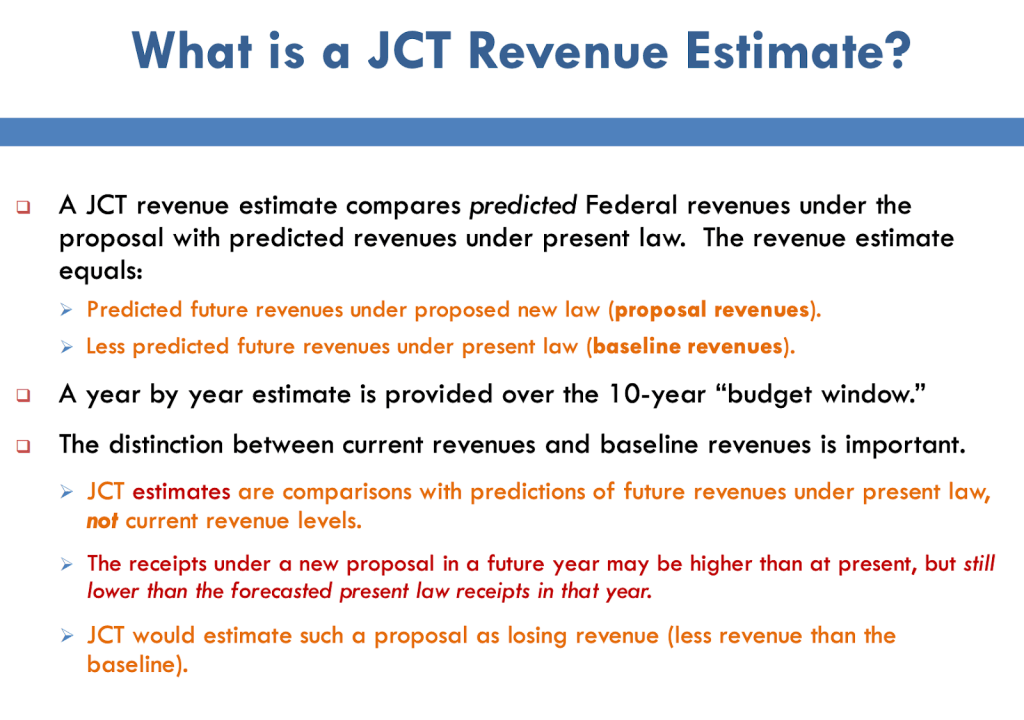

- Joint Committee on Taxation projects federal receipts under proposed legislation

- jct.gov/about-us/revenue-estimating.html

- The starting point for a revenue estimate prepared by the Joint Committee staff is the Congressional Budget Office (“CBO”) 10-year projection of Federal receipts, referred to as the “revenue baseline.” The revenue baseline serves as the benchmark for measuring the effects of proposed tax law changes. The baseline assumes that present law remains unchanged during the 10-year budget period. Thus, the revenue baseline is an estimate of the Federal revenues that will be collected over the next 10 years in the absence of statutory changes.

- The Joint Committee staff uses confidential tax return information to prepare revenue estimates.

- The Joint Committee staff uses several highly developed microsimulation tax models to estimate the revenue impact of changes in tax laws

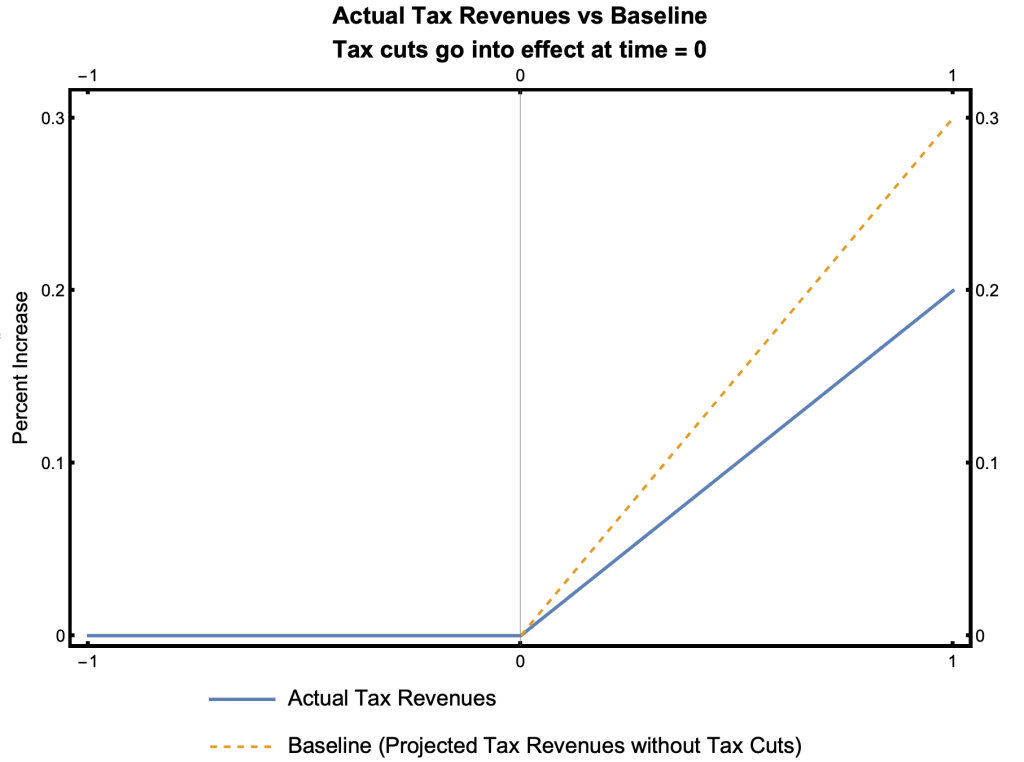

Baselines

- Scenario

- The government reduces tax rates and the following year tax revenues increase by 2%. It would seem that the effect of the tax cuts was to increase tax revenues by 2%.

- But …

- Tax cuts were projected to grow at 3% without the tax cuts. The effect of the tax cuts was thus to reduce tax revenues relative to what they would been otherwise, i.e. relative to the baseline.

Generated by Mathematica, Descriptive Statistics.nb

Did Trump’s tax cuts pay for themselves?

Federal revenues rose by 0.4 percent from the 2017 fiscal year to the 2018 fiscal year. It was argued that Trump’s tax cuts thus paid for themselves in fiscal 2018, by bringing in more tax revenue than in the preceding year.

Analysis by Jim Tankersley

No, Trump’s Tax Cut Isn’t Paying for Itself (at Least Not Yet)

- Technical objection 1

- Fiscal year is the wrong time frame. Fiscal year 2018 started in October 2017, three months before the tax cuts went into effect. So the first quarter doesn’t count. From January through September 2017, revenues were $2.57 trillion. For the same period in 2018, they were $2.56 trillion. Which is to say, they’re down by $10 billion, in a direct comparison after the tax cuts started.

- Technical objection 2

- Inflation has to be factored in, In real dollars tax revenues were down in 2018 even more than $10 billion

- Main objection

- The real issue is: Have the corporate and individual tax cuts that went into effect in January generated so much additional growth that tax revenues are as high, or higher, today than they would have been if the tax cuts never passed? That’s how all scorekeepers — be they independent congressional staff members or researchers from think tanks that lean liberal or conservative — assess the “pay for themselves” question

- One way to think about it is from the perspective of a small-business owner. Let’s say you run your own bakery. You sell bread for $4 a loaf. Today, you sold 90 loaves, for $360 in revenue. You expect that, because it’s a busier day at the bakery tomorrow, you’ll sell 100 loaves then, earning $400. But you’d like to sell even more than that, so you lower the price to $3 a loaf to encourage additional purchases.

- Congratulations! You sell 125 loaves. Your revenue goes up, to $375. That’s more than you brought in the day before. Your price cut, though, has not “paid for itself” — because you ended up bringing in less revenue than you would have otherwise.

- In other words, you brought in more money than the day before. But it’s less than you would have made if you hadn’t cut the price.

- That’s what we saw in the 2018 fiscal year with the tax cuts. A few months before they passed, the Congressional Budget Office predicted the government would take in $3.53 trillion in revenues for the fiscal year. On Monday, the Treasury reported that revenue was actually $3.33 trillion for the year — $200 billion short, even though economic growth has outpaced the budget office’s forecasts.

- That’s the equivalent of selling more loaves, but earning less money.

Percent Change in After-tax Income

- William Gale of TPC argues that the best way to measure the impact of a tax cut on individual taxpayers is by examining how a tax affects a household’s after-tax income.

- The idea is to compute how much of a raise a person gets.

- If a person’s after-tax income increases from $100K to $110K, they got a 10% government raise.

- He offered this example. (Is the Trump tax cut good or bad for the middle class?)

- Assume a person has:

- $100 in income

- $1 in income tax

- $10 in other federal taxes, such as Social Security

- Suppose the tax bill cuts his income tax to zero. Then:

- His income tax goes down by $1, so his income tax goes down by 100 percent

- His federal tax goes down by $1, so his federal tax goes down by 9 percent

- His after-tax income goes up by $1, so his after-tax income goes up by 1.12 percent (90/89 = 1.0112).

- The third result is the most informative:

- He got a 1.12% government raise.

- Assume a person has:

Addenda

Forecasting Effects of Tax Bills

- Computer Models

- Joint Committee on Taxation, jct.gov/

- The nonpartisan Joint Committee Staff is a congressional agency responsible for providing the U.S. Congress with the budgetary effects of all tax legislation.

- Tax Policy Center, taxpolicycenter.org/

- Penn-Wharton Budget Model, budgetmodel.wharton.upenn.edu/tax-policy/

- Tax Foundation, taxfoundation.org/

- Joint Committee on Taxation, jct.gov/

- Historical Evidence

- Reagan tax cuts of 1981 and 1986

- Clinton tax increase of 1993

- Bush’s tax cuts of 2001 and 2003

- Obama tax cuts of 2010 and 2013

- Kansas Experiment of 2013-2017

- Economists Opinion: IGM Forum

JCT on the Baseline

Baseline Analogy

- Consider for fun the claim that the tax cuts brought about an increase in the number of people employed. Looking at the Payroll Survey Line, you see that the number of people employed in July 2018 is greater than the number employed when the tax cuts passed. Case Closed?

- But wait a second. The trend had been in the same upward direction since 2013. So if the tax cuts had an effect on the number of people employed, the Payroll Survey Line should have bent upwards after the tax cuts. But the line didn’t change direction. So the tax cuts had no effect.

- Whether the tax cuts had an effect is determined by comparing the actual change with the change that would have occurred with no tax cuts.

Tax Resources Recommended by Bruce Bartlett

- Congressional Budget Office (CBO)

- Joint Committee on Taxation (JCT)

- U.S. Government Accountability Office (GAO)

- National Bureau of Economic Research (NBER)

- Department of the Treasury Tax Policy

- Tax Policy Center (TPC)

- Tax Foundation (TF)

- Congressional Research Service [CRS] Reports

- Organization for Economic Cooperation and Development in Paris (OECD)

- IRS SOI Bulletins