Table of Contents

- Debt Limit Crises versus Shutdowns

- Debt Limit Reached January 2023

- House Speaker and Minority Leader on the Crisis

- Possible Outcomes

- Extraordinary Measures

- History of the Debt Ceiling and Recent Crises

- More on Outcomes

- The Debt Limit as a Political Weapon

- Biden could just as easily extort House Republicans

- Attempted Extortion

- National Debt

- The Baseline Problem

- Three Ways to View Interest on the National Debt

- The End

- Reducing the Debt

Debt Limit Crises versus Shutdowns

Debt Limit Crises and 31 U.S. Code §3101

- The amount of the government’s public debit is limited by statute.

- 31 U.S. Code § 3101 – Public debt limit

- The face amount of obligations issued under this chapter and the face amount of obligations whose principal and interest are guaranteed by the United States Government (except guaranteed obligations held by the Secretary of the Treasury) may not be more than [$31,381,463,000,000] outstanding at one time, subject to changes periodically made in that amount as provided by law through the congressional budget process.

- 31 U.S. Code § 3101 – Public debt limit

- A debt ceiling crisis occurs when the debt limit is reached, requiring the Treasury to take extraordinary measures to prevent the US from defaulting on its obligations.

- A government default occurs when the debit limit binds, meaning that the Treasury can no longer meet all its financial obligations.

fiscaldata.treasury.gov/americas-finance-guide/national-debt/

The U.S. Treasury uses the terms “national debt,” “federal debt,” and “public debt” interchangeably.

There are two major categories of federal debt: debt held by the public and intragovernmental holdings.

Shutdowns and Appropriation Bills

- Congress passes Appropriations Bills that appropriate funds from the Treasury for government agencies and departments.

- Consolidated Appropriations Act, 2023 (the 1.7 trillion omnibus appropriations bill).

- The following sums in this Act are appropriated, out of any money in the Treasury not otherwise appropriated, for the fiscal year ending September 30, 2023.

- OFFICE FOR CIVIL RIGHTS

- For expenses necessary for the Office for Civil Rights, as authorized by section 203 of the Department of Education Organization Act, $140,000,000.

- OFFICE OF INSPECTOR GENERAL

- For expenses necessary for the Office of Inspector General, as authorized by section 212 of the Department of Education Organization Act, $67,500,000, of which $3,000,000 shall remain available until expended.

- OFFICE FOR CIVIL RIGHTS

- The following sums in this Act are appropriated, out of any money in the Treasury not otherwise appropriated, for the fiscal year ending September 30, 2023.

- Consolidated Appropriations Act, 2023 (the 1.7 trillion omnibus appropriations bill).

- A government shutdown happens when departments of the government shut down because funds have not been appropriated for those departments for the fiscal year.

- The most significant shutdowns:

- 21-day shutdown of 1995–1996 during the Bill Clinton administration over spending cuts pushed by Congressional Republicans

- 16-day shutdown in 2013 during the Barack Obama administration over Republican demands to defund Obamacare.

- The shutdown was accompanied by a debt ceiling crisis.

- 35-day shutdown of 2018-2019 during the Donald Trump administration (the longest shutdown in US history) over funding for the border wall.

Debt Limit Reached January 2023

- From Yellen’s January 13th Letter to Congressional Leadership

- Public Law 117-73 increased the statutory debt limit to approximately $31.381 trillion on December 16, 2021.

- I am writing to inform you that beginning on Thursday, January 19, 2023, the outstanding debt of the United States is projected to reach the statutory limit. Once the limit is reached, Treasury will need to start taking certain extraordinary measures to prevent the United States from defaulting on its obligations.

- Increasing or suspending the debt limit does not authorize new spending commitments or cost taxpayers money. It simply allows the government to finance existing legal obligations that Congresses and Presidents of both parties have made in the past.

- The Treasury estimates that the extraordinary measures will be sufficient at least through early June.

- C.B.O. Warns of Possible Default Between July and September NYT

House Speaker and Minority Leader on the Crisis

- Kevin McCarthy, Speaker of the House

- “I want to find a reasonable and responsible way that we can lift the debt ceiling but take control of this runaway spending”

- “Cuts to Medicare and Social Security, they are off the table”

- “Look, we’re not going to default.”

- “We will not agree to a debt limit increase absent a discretionary budgetary agreement in line with the House-passed budget resolution or other commensurate fiscal reforms to reduce and cap the growth of spending.”

- Promise made to the Freedom Caucus, per Susan Ferrechio of the Washington Times Vox

- Hakeem Jeffries, House Minority Leader

- “There is a difference between a compromise and a ransom note. And so let me be clear. We are not going to pay a ransom note to extremists in the other party” NPR

Possible Outcomes

- The House passes a debt ceiling increase or suspension with no conditions

- Kevin McCarthy concedes

- Democrats and some Republicans initiate a discharge petition (View More)

- Democrats make a deal with Republicans

- Democrats agree to real spending cuts

- Democrats make pseudo-concessions, allowing McCarthy to save face.

- The Treasury defies the debt ceiling

- Treasury invokes the Fourteenth Amendment (View More)

- Treasury argues the debt ceiling conflicts with appropriations already enacted. (View More)

- The Treasury uses exotic methods to raise cash

- Mint a trillion dollar platinum coin. (View More)

- Sell interest-only bonds (View More)

- The Treasury defaults on some of its obligations. (View More)

Extraordinary Measures

- The Treasury has taken “extraordinary measures” to delay default.

- The basic idea is robbing Peter (government investment funds) to pay Paul (current debts).

- From Yellen’s January 13th Letter to Congressional Leadership

- The two extraordinary measures Treasury anticipates implementing this month [January] are

- Redeeming existing, and suspending new, investments of the Civil Service Retirement and Disability Fund (CSRDF) and the Postal Service Retiree Health Benefits Fund (Postal Fund)

- Suspending reinvestment of the Government Securities Investment Fund (G Fund) of the Federal Employees Retirement System Thrift Savings Plan.

- After the debt limit impasse has ended, the CSRDF, Postal Fund, and G Fund will be made whole.

- The two extraordinary measures Treasury anticipates implementing this month [January] are

- Treasury Department on Extraordinary Measures

History of the Debt Ceiling and Recent Crises

- Sundry Facts

- A debt limit was first enacted in 1917

- The first aggregate debt limit was enacted in 1939.

- Congress has approved 102 debt limit modifications since the end of World War II

- The debt limit was raised to its current level in December 2021 when Democrats passed legislation 50-49 in the Senate and 221-209 in the House. The only Republican to vote for the increase was Adam Kinzinger.

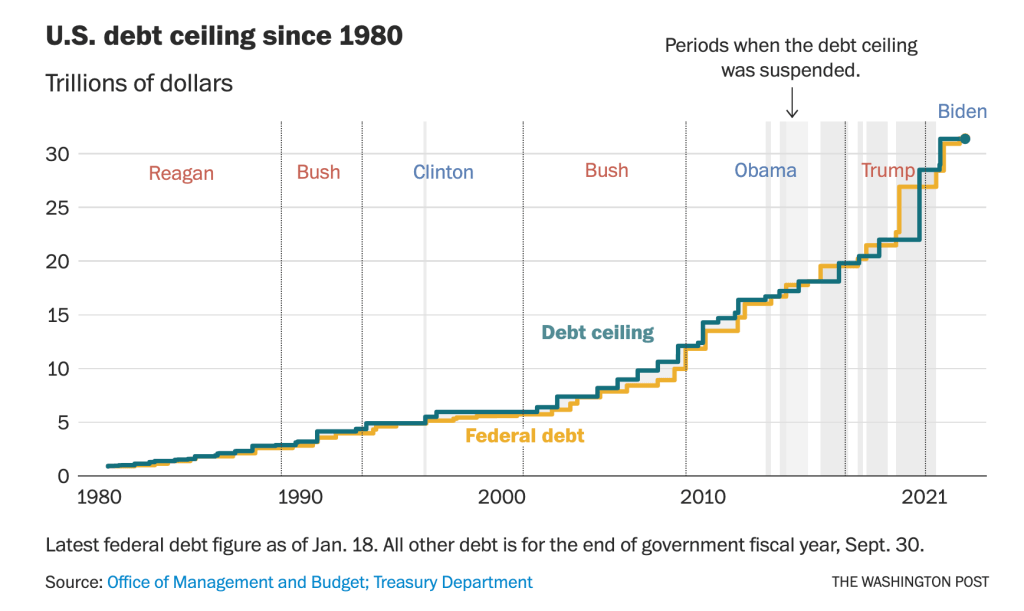

- Debt Limit since 1980

- Query:

- How can the yellow line be above the green line, e.g. during the Trump administration?

- Query:

- Recent Debt Limit Crises

- 2011 – Hours to Deadline

- 2013 – One Day to Deadline

- 2017 – Weeks to Deadline

- 2018 – One Month to Deadline

- 2019 – One Month to Deadline

- 2021 – Weeks to Deadline

- Really Close Debt Limit Crises

- 2011 Hours to Deadline

- Congressional Republicans used the debt ceiling as leverage for deficit reduction.

- Obama negotiated with Republicans, resulting in the Budget Control Act of 2011 and the 2013 Budget Sequestration.

- 2013 One Day to Deadline

- Congressional Republicans refused to raise the debt ceiling unless Obama agreed to defund the Affordable Care Act

- Obama refused and Republicans raised the debt ceiling.

- 2011 Hours to Deadline

More on Outcomes

Defaulting on its Obligations

- From Yellen’s January 13th Letter to Congressional Leadership

- Failure to meet the government’s obligations would cause irreparable harm to the U.S. economy, the livelihoods of all Americans, and global financial stability. Indeed, in the past, even threats that the U.S. government might fail to meet its obligations have caused real harms, including the only credit rating downgrade in the history of our nation in 2011.

- Congressional Research Service CRS

- Possible consequences of a binding debt limit include, but are not limited to, the following:

- reduced ability of Treasury to borrow funds on advantageous terms, thereby further increasing federal debt;

- substantial negative outcomes in global economies and financial markets caused by anticipated default on Treasury securities or failure to meet other legal obligations;

- acquisition of interest penalties from delay on certain federal payments and transfers;

- downgrades of U.S. credit ratings, which could negatively impact capital markets.

- Possible consequences of a binding debt limit include, but are not limited to, the following:

- Debt Limit Brinkmanship (Again), Moody’s Analytics

- If lawmakers are unable to resolve the debt limit in time and the Treasury begins paying its bills late and defaults, financial markets would be roiled. A TARP moment seems likely, hearkening back to that dark day in autumn 2008 when Congress initially failed to pass the Troubled Asset Relief Program bailout of the banking system, and the stock market and other financial markets cratered.

- It is unimaginable that lawmakers would allow things to get to this point, but as the TARP experience highlights, they have done the unimaginable before.

- How worried should we be if the debt ceiling isn’t lifted? Brookings Institute

- While greatly uncertain, the effects of allowing the debt limit to bind could be quite severe, even assuming that principal and interest payments continue to be made. If instead the Treasury fails to fully make all principal and interest payments—because of political or legal constraints, unexpected cash shortfalls, or a failed auction of new Treasury securities—the consequences would be even more dire.

- The workarounds that have been proposed—the platinum coin, borrowing anyway, prioritizing payments—either bring significant legal uncertainty or are not sustainable solutions. These unlikely workarounds do not avoid the chaos that is inherent to the debt ceiling binding. The only effective solution is for Congress to increase the debt ceiling or, better yet, abolish it.

- How will the U.S. Treasury operate when the debt limit binds? Brookings Institute

- One cannot predict how Treasury will operate when the debt limit binds, given that this would be unprecedented. Treasury did have a contingency plan in place in 2011 when the country faced a similar situation, and it seems likely that Treasury would follow the contours of that plan if the debt limit were to bind this year. Under the plan, there would be no default on Treasury securities. Treasury would continue to pay interest on those Treasury securities as it comes due. And, as securities mature, Treasury would pay that principal by auctioning new securities for the same amount (and thus not increasing the overall stock of debt held by the public). Treasury would delay payments for all other obligations until it had at least enough cash to pay a full day’s obligations. In other words, it will delay payments to agencies, contractors, Social Security beneficiaries, and Medicare providers rather than attempting to pick and choose which payments to make that are due on a given day.

Some Republicans Working with Democrats

Using a Discharge Petition

- The discharge petition won’t save us, Joshua Huder, WaPo

- It’s technically possible that a handful of House Republicans representing swing districts could band with Democrats to force a vote on a clean debt ceiling hike, employing a rarely used maneuver known as a discharge petition. But this would require a lot of precise parliamentary maneuvering over the heads of House GOP leaders, not to mention a surprising degree of bipartisan cooperation.

- The discharge process, established in 1910, enables a majority of the House to sidestep the speaker and committee chairs to push forward needed legislation on their own. Because it allows a majority of the House to circumvent committees and the speaker, the mechanism was meant as a sort of emergency release valve. If House leaders refused to bring a popular bill to a vote, rank-and-file members had a means to go around them.

- So far so good — except it won’t be of much use in dealing with the debt limit. There is a twofold problem.

- First, discharge is an extremely slow process: A given bill must sit in committee for 30 legislative days. Then 218 House members have to sign a petition calling for it to be “discharged” to the floor. Then that petition needs to sit on a House calendar for seven legislative days. And only then can a member bring the bill to a vote.

- Second, the discharge process is clumsy. For it to work, this rogue majority of House members would need to strike a deal with Senate leaders far in advance, then pass that deal through both chambers without changes — or the House members who discharged the bill lose control of it to the speaker.

- At core, there is no getting around the fact that both a discharge process and renegade floor action would represent partisan heresy.

- The reasons discharge petitions succeed only 2 percent of the time is the same reason that cross-partisan alliances don’t hijack the House floor: The political cost of turning your back on your colleagues is too high.

Defying the Debt Ceiling

Invoking the Fourteenth Amendment

- Public Debt Clause of the Fourteenth Amendment (Section 4)

- The validity of the public debt of the United States, authorized by law, including debts incurred for payment of pensions and bounties for services in suppressing insurrection or rebellion, shall not be questioned.

- Paraphrase:

- The integrity of the public obligations of the US shall not be challenged

- Perry v US (1935)

- “Nor can we perceive any reason for not considering the expression ‘the validity of the public debt’ as embracing whatever concerns the integrity of the public obligations.”

- Perry v US (1935)

- The integrity of the public obligations of the US shall not be challenged

- The argument:

- The Treasury’s letting the US default on its financial obligations challenges the integrity of the public obligations of the US.

- It is unconstitutional to challenge the integrity of the public obligations of the US.

- Therefore, it is unconstitutional for the Treasury to let the US default on its financial obligations.

- In its 2021 report, the Congressional Research Service noted that this part of the Constitution has been tested only once by the Supreme Court, adding that it is “unclear how the provision might apply to the statutory debt limit in particular.”

- Related Argument:

- Lawrence Tribe, Harvard law professor says: “Section 4 of the 14th Amendment says the threat to default is itself unconstitutional.”

- The Argument:

- Threatening to let the US default on its financial obligations challenges the integrity of the public obligations of the US.

- It is unconstitutional to challenge the integrity of the public obligations of the US.

- The Republican-led House is threatening to let the US default on its financial obligations

- Therefore, the Republican-led House’s threat is unconstitutional.

Choosing between Conflicting Laws

- 31 U.S. Code § 3102 through 31 U.S. Code § 3106 authorize the Secretary of the Treasury to borrow money to pay authorized expenditures.

- 31 U.S. Code § 3101 prohibits the Treasury from borrowing more than the debt limit.

- But these laws conflict when the debt limit binds.

- Under such circumstances the Secretary may choose either prohibited course of action.

- Alternative view:

- Under such circumstances the Secretary should ignore the debt limit.

- Neil H. Buchanan and Michael C. Dorf argue that the president should choose the “least unconstitutional” course: ignoring the debt ceiling

- Under such circumstances the Secretary should ignore the debt limit.

Using Exotic Methods to Raise Cash

Minting a Trillion Dollar Platinum Coin

- The idea is that the Treasury Secretary, per 31 US Code § 5112, could instruct the US Mint to make a $1 trillion platinum coin and then deposit it in Treasury’s General Account at the Federal Reserve.

- 31 U.S. Code § 5112 – Denominations, specifications, and design of coins (enacted 1997)

- (k) The Secretary may mint and issue platinum bullion coins and proof platinum coins in accordance with such specifications, designs, varieties, quantities, denominations, and inscriptions as the Secretary, in the Secretary’s discretion, may prescribe from time to time.

- But there is no guarantee the Fed will accept the coin.

- A platinum commemorative coin from the US Mint:

Selling Federal Land

- The government could auction off federal land and buy it back later.

Asking the Fed for an Advance

- The Federal Reserve routinely sends the Treasury income from interest payments on government bonds the Fed holds on its balance sheet. There’s nothing preventing the Fed from paying the Treasury in advance, according to economist J.W. Mason.

Selling Interest-only Bonds

- The public national debt includes the principal of outstanding Treasuries but not the interest to be paid.

- So the Treasury could sell bonds that pay interest but never mature.

- “With this kind of bond, there is no principal the government is guaranteed to repay,” Carlos Mucha said. “So it would not count under the debt limit.”

Buying Back Old Bonds at a Discount

- The Treasury could repurchase government bonds, issued with lower interest rates, on the secondary market for less than their face value (because the Federal Reserve has since raised interest rates). If the Treasury buys back a $10,000 bond for $9,000, the national debt is reduced by $10,000. Then it issues a new $10,000 bond. So the national debt remains the same, but the Treasury netted $1,000 in cash.

The Debt Limit as a Political Weapon

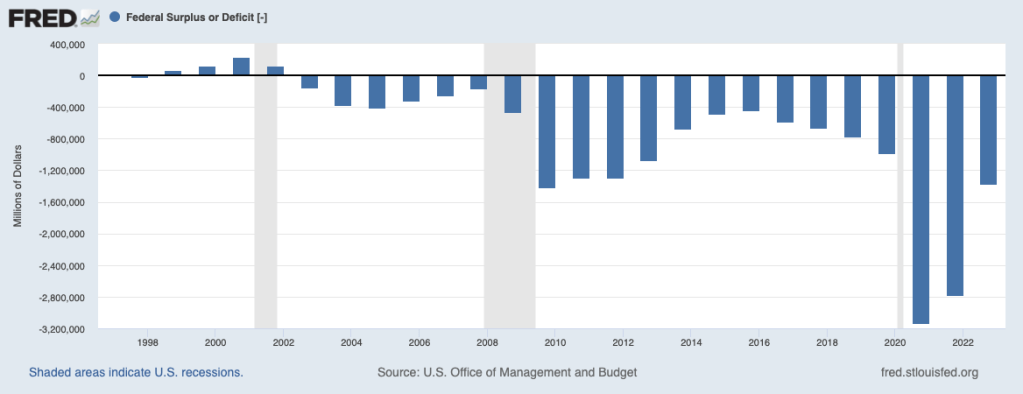

- For the past 22 years, under both Democrats and Republicans, the Federal government has run deficits. (The last Federal surpluses were in 1998 through 2001.)

- It appears that Democrats are more interested in expanding government programs and Republicans more interested in cutting taxes than either is in reducing the debt.

- It’s thus disingenuous of a party that controls a branch of Congress to demand either spending cuts or raising taxes to reduce the debt only when the president is a member of the opposite party.

- wikipedia.org/wiki/Economic_policy_of_the_Bill_Clinton_administration

- The 1998-2001 surpluses were attributed to a strong economy generating high tax revenues, tax increases on upper-income taxpayers, spending restraint, and capital gains tax revenue from a stock market boom. (Factcheck.org)

- This pattern of raising taxes and cutting spending (i.e., austerity) in an economic boom coincides precisely with the advice of John Maynard Keynes, who stated in 1937: “The boom, not the slump, is the right time for austerity at the Treasury.” (Krugman)

Biden could just as easily extort House Republicans

- The House Republicans are trying to get Democrats to agree to spending cuts by threatening that they, the Republicans, will not pass legislation to raise the debt ceiling unless the Democrats agree to the cuts. That is, they are trying to extort spending cuts from the Democrats.

- “Extort” means to get something by force or threats (Cambridge Dictionary)

- But Biden, if he wanted, could try to extort House Republicans, for example, by threatening to veto any bill increasing the debt ceiling that doesn’t also reduce the debt by raising taxes on the wealthy.

Attempted Extortion

- Hakeem Jeffries:

- “There is a difference between a compromise and a ransom note. And so let me be clear. We are not going to pay a ransom note to extremists in the other party”

- Catherine Rampell (WaPo) makes the following analogy:

- “Imagine if Republican lawmakers threatened to blow up the Washington Monument unless Democrats agreed to cut Social Security. Pretty much the same form of extortion is happening right now, only the bomb is aimed at a different target: the global economy.”

- “Extort” means to get something by force or threats (Cambridge Dictionary)

National Debt

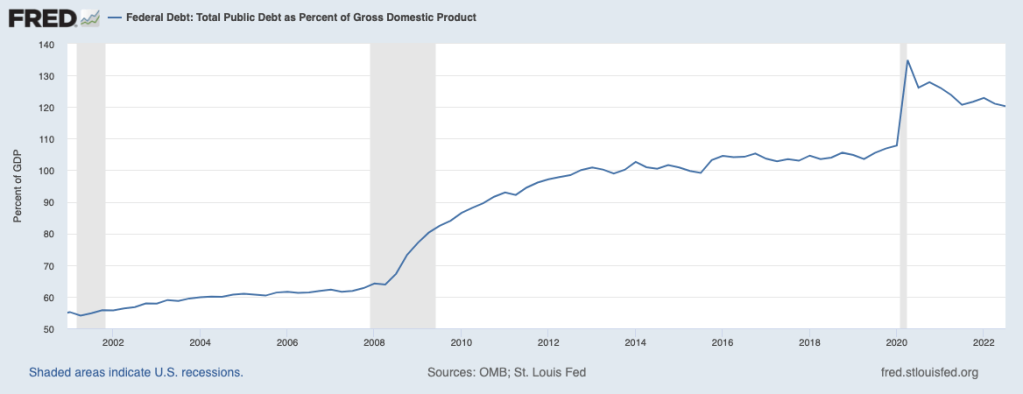

- Federal Debt: Total Public Debt as Percent of Gross Domestic Product

- Debt as % of GDP increases during Great and Covid Recessions.

fred.stlouisfed.org/series/GFDEGDQ188S#0

- Paul Krugman NYT

- Most of the debt was incurred during two episodes:

- the 2007-9 Great Recession and its aftermath

- the Covid-19 pandemic.

- Great Recession:

- In the case of the recession, the deficit shot up largely because tax receipts plunged along with the economy, while social safety net spending, especially unemployment benefits, soared. Barack Obama’s stimulus package was also a factor, but it was only part of the story.

- Covid Recession:

- Then came Covid, and this time the government responded very strongly, with trillions in aid to families, businesses, the unemployed and state and local governments. The result was a gratifyingly fast economic recovery — again, accompanied by a burst of inflation, but that seems to be subsiding. Of course, there was also a jump in debt.

- Most of the debt was incurred during two episodes:

- How the U.S. Government Amassed $31 Trillion in Debt Jim Tankersley NYT

- America’s ballooning debt is the result of choices made by both Republicans and Democrats. Since 2000, politicians from both parties have made a habit of borrowing money to finance wars, tax cuts, expanded federal spending, care for baby boomers, and emergency measures to help the nation endure two debilitating recessions.

- The biggest — and often bipartisan — drivers of debt have been the federal responses to two sharp economic downturns:

- the 2008 financial crisis

- the 2020 pandemic recession.

- U.S. on Track to Add $19 Trillion in New Debt Over 10 Years NYT

- The United States is on track to add nearly $19 trillion to its national debt over the next decade, $3 trillion more than previously forecast, as a result of rising costs for interest payments, veterans’ health care, retiree benefits and the military, the Congressional Budget Office said on Wednesday.

The Baseline Problem

- Suppose legislation is proposed to reduce the debt, either by cutting spending, raising taxes, or both. The Congressional Budget Office evaluates legislation by comparing its projected consequences with the baseline of the projected consequences of no legislation.

- The problem is that no one knows what the baseline future is.

- Brookings Institute

- No one really knows at what level a government’s debt begins to hurt an economy; there’s a heated debate among economists on that question.

- The federal debt cannot grow faster than the economy indefinitely. Eventually, private borrowing will be crowded out if the government’s debt continues to grow, and interest rates will rise. At some point, action will have to be taken to rein in the deficit, but we may be a long way from that point.

- Brookings Institute

- There is no reliable way of determining whether a piece of debt-reduction legislation will make the economy better or worse in the long run.

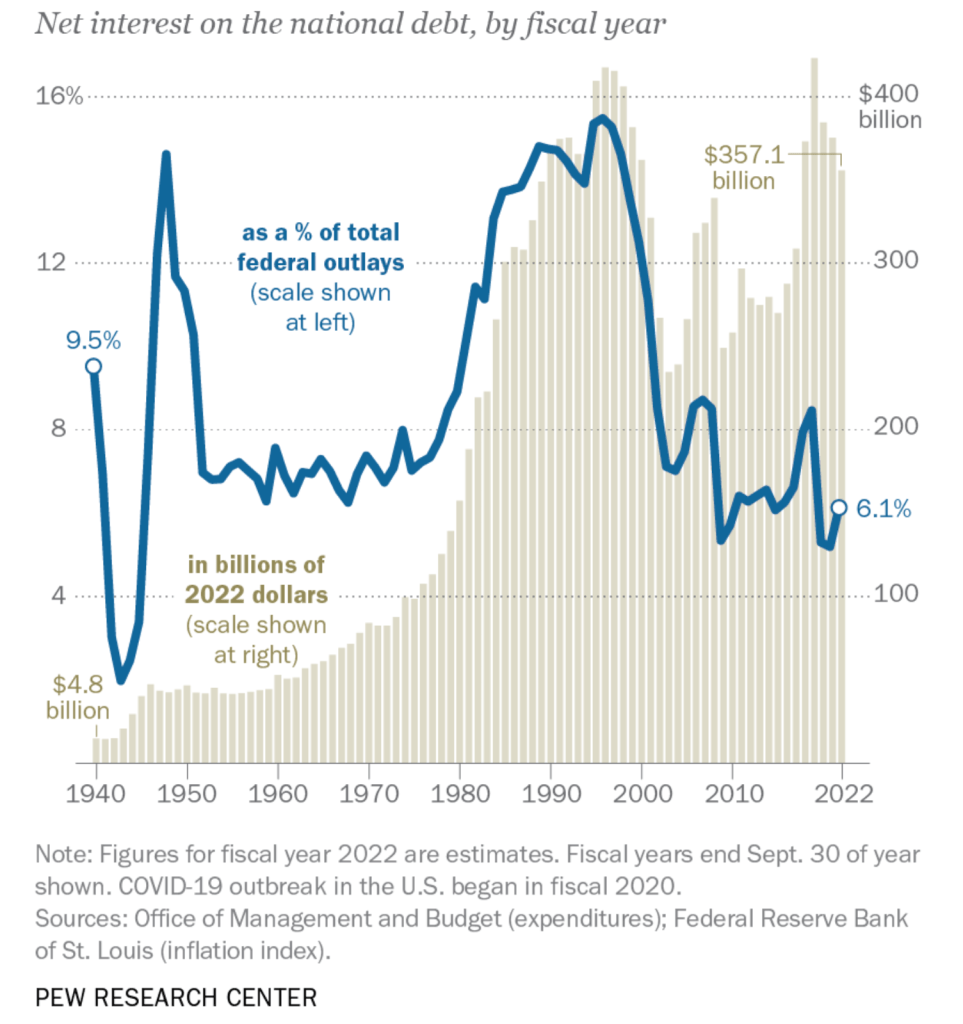

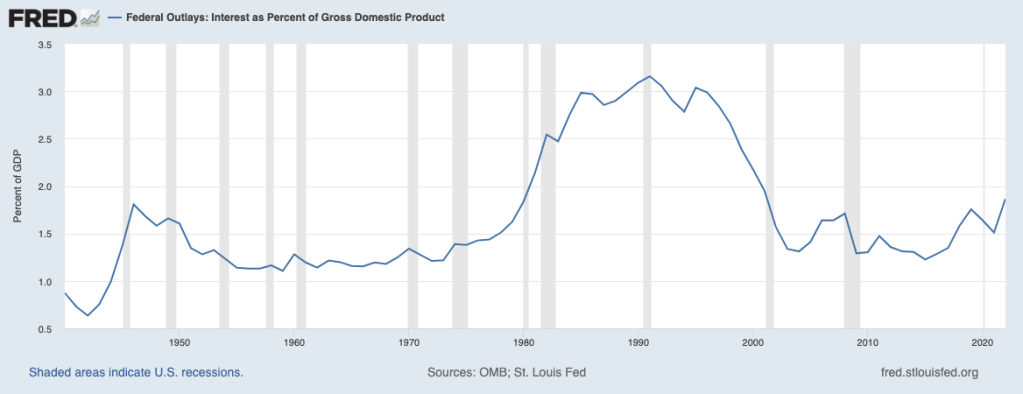

Three Ways to View Interest on the National Debt

Dollar Amount of Interest

fred.stlouisfed.org/series/FYOINT

Interest as a Percent of Total Outlays

pewresearch.org/fact-tank/2023/02/14/facts-about-the-us-national-debt

Interest as a Percent of GDP

fred.stlouisfed.org/series/FYOIGDA188S#

The End

- An Analogy:

- The US population will eventually reach a point where it can no longer be supported by the economy. Action should be taken now, rather than later, to prevent such a population crisis, for example, limiting families to three children.

- The national debt will eventually reach a point where there are insufficient funds to keep the government operating. Action should be taken now, rather than later, to prevent such a fiscal crisis, for example phasing out Social Security, Medicare, and Medicaid.

Reducing the Debt

- Please Don’t Feed the Debt Scolds Paul Krugman NYT

- In March 2011 Erskine Bowles and Alan Simpson, chairs of a White House deficit-reduction commission, issued a frightening warning about U.S. government debt. Unless America took major steps to rein in future deficits, they warned, a fiscal crisis could be expected within around two years.

- There was an elite consensus at the time that budget deficits were a severe, even existential threat. This consensus was, in retrospect, completely wrong

- It’s true that U.S. debt is very large — $31 trillion (said in your best Dr. Evil voice). But America is a big country, so almost every economic number is very large. A better way to think about debt is to ask whether interest payments are a major burden on the budget. In 2011 these payments were 1.47 percent of gross domestic product — half what they had been in the mid-1990s. In 2021 they were 1.51 percent. This number will rise as existing debt is rolled over at higher interest rates, but real net interest — interest payments adjusted for inflation — is likely to remain below 1 percent of G.D.P for the next decade.

fred.stlouisfed.org/series/FYOIGDA188S#

- The Decision Problem:

- Consider a proposal to seriously reduce or eliminate deficits over the next ten years, whether by increasing taxes, cutting programs, or both.

- Rational decision making requires comparing the projected human and economic consequences of the proposal with those of the status quo.

- The CBO can project the consequences of deficit reduction. But what are the consequences of the status quo? Will it lead to a fiscal crisis in two years, five years, 10 years, or never?

- Paul Krugman NYT

- In March 2011 Erskine Bowles and Alan Simpson, chairs of a White House deficit-reduction commission, issued a frightening warning about U.S. government debt. Unless America took major steps to rein in future deficits, they warned, a fiscal crisis could be expected within around two years.

- Paul Krugman NYT

- Paul Krugman NYT

- The fundamental fact about the budget is that the federal government is basically an insurance company with an army. Social Security, Medicare, Medicaid and the military dominate spending, and it’s impossible to do much about deficits unless you either raise taxes or make major cuts to these programs.

- Philip Bump WaPo

- According to an analysis by the Committee for a Responsible Federal Budget (CRFB), to balance the budget without increasing revenue — mostly meaning taxes — you’d need to trim the federal budget by 26 percent over the next decade. If you exclude defense and veterans programs from cuts, you need to eliminate a third of what’s left. Take out Social Security and Medicare, too, and suddenly you have to cut basically everything.

- The Programs You’d Have to Cut to Balance the Budget NYT Upshot March 2023