- Monte Carlo Simulation for Standard Errors of IV and intercept

- Linear Regression on GDP and IMF

- NonLinear Regression on GDP and IMF

- Linear Regression on GDP and Redundant GDP (1/3 times GDP)

- Linear Regression on GDP, IMF, and Gini

- NonLinear Regression on GDP, IMF, and Gini

- Linear Regression on GDP

- Linear Regression on Random Numbers

- Linear Regression on

Monte Carlo Simulation for Standard Errors of IV and intercept

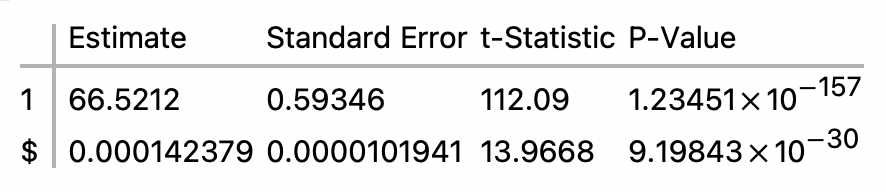

- For the Linear Regression on GDP:

- The data consists of 167 paired x’s and y’s

- The regression is: y = 66.5212 + 0.000142379 $

- The Parameter Table is

- A Monte Carlo simulation, run with 10,000 iterations, estimated the standard errors as

- Standard error of intercept = 0.593747

- Standard error of the variable $ = 0.0000102458

- Monte Carlo simulation for finding the standard error in general

- Define the population parameter for which the standard error is sought.

- Loop thousands of times:

- Take an n-size random sample from the population

- Compute the statistic of interest for the sample

- Store the computed sample statistic

- End Loop

- The standard error is approximated by the SD of all the computed sample statistics.

- Monte Carlo simulation for finding the standard errors for IV and intercept

- Define the dataset and regression for which standard errors are sought.

- We’ll call these the given dataset and the given regression

- Loop thousands of times:

- Generate a dataset of random x’s and y’s analogous to the x’s and y’s of the given dataset (this is the tricky part — see below)

- Do a regression on the analogous dataset

- Store the a and b coefficients of the regression equation

- End Loop

- Calculate the SD of all the a coefficients — that approximates the standard error of the intercept

- Calculate the SD of the all b coefficients — that approximates the standard error of the IV

- The Tricky part

- We want make a dataset of x’s and y’s relevantly like, but not identical with, the x’s and y’s of the given dataset.

- The x’s are easy: Use random numbers from the normal distribution with mean and SD of the given x’s.

- The y’s are tricky: A y has to bear approximately the same relation to its paired x as do the given y’s to their paired x’s.

- First, use the given regression equation, and the random x, to compute a predicted y.

- Then get a random residual from the normal distribution with mean and SD of the given residuals.

- The y you want is the predicted y minus the random residual.

- Mathematica Code

- big$iterations = 10000;

- bigout = List[];

- dc = Length[regress[“Data”]];

- serorig = Sqrt[Total[regress[“FitResiduals”]^2]/(dc-(1+1))];

- sdforx=Sqrt[N[Total[Table[(regress[“Data”][[i,1]] – Mean[regress[“Data”][[All,1]]])^2,{i,1,dc}]]]/(dc -(1+1))];

- meanforx =N[Mean[regress[“Data”][[All,1]]]];

- Do[

- inside$iterations = dc;

- sampstat = List[];

- Do[

- resrand=RandomVariate[NormalDistribution[0,serorig]];

- xrand = RandomVariate[NormalDistribution[meanforx, sdforx]];

- predicty=regress[“Function”][xrand];

- observedy=predicty-resrand;

- sampstat =Append[sampstat, {xrand,observedy} ];,

- {inside$iterations}];

- sampregress=LinearModelFit[sampstat,x,x];

- tmpa=sampregress[“ParameterTableEntries”][[1,1]];

- tmpb=sampregress[“ParameterTableEntries”][[2,1]];

- bigout =Append[bigout, {tmpa,tmpb} ];,

- {big$iterations}]

- regress[“ParameterTable”]

- StandardDeviation[bigout[[All,1]]]

- StandardDeviation[bigout[[All,2]]]

Linear Regression on GDP and IMF

- Regression Equation; y = 68.4357 – 40.3304 m + 0.000124256 $

- DataPoints = 167

- NbrofIVs = 2

- Sum of Squares Equation: 5912.8 + 3764.14 = 9676.95

- SSR + SSE = SST, where SSR, SSE, and SST are the sums of squares for

- predicted y’s

- residuals

- observed y’s

- Standard Error of the Regression = 4.79083

- = √(SSE / (Datapoints – (NbrofIVs + 1)))

- R-Squared = 0.61102

- Adjusted R-Squared = 0.606276

- AICc = 1002.45

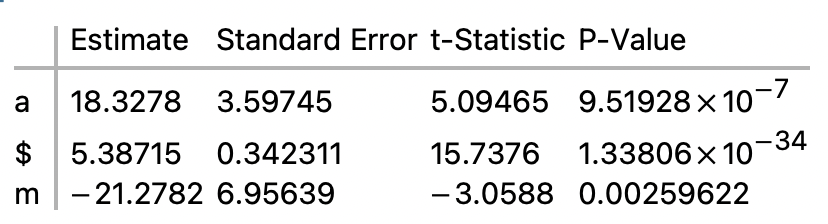

NonLinear Regression on GDP and IMF

- Regression Equation; y = 18.3278 – 21.2782 y + 5.38715 Log[x]

- DataPoints = 167

- NbrofIVs = 2

- Sum of Squares Equation: 6765.65 + 2911.3 = 9676.95

- SSR + SSE = SST, where SSR, SSE, and SST are the sums of squares for

- predicted y’s

- residuals

- observed y’s

- Standard Error of the Regression = 4.21329

- = √(SSE / (Datapoints – (NbrofIVs + 1)))

- R-Squared = 0.699151

- Adjusted R-Squared = 0.695482

- AICc = 959.546

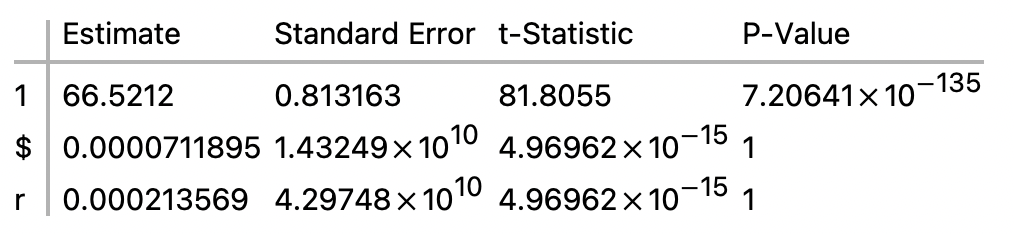

Linear Regression on GDP and Redundant GDP (1/3 times GDP)

- Regression Equation; y = 66.5212 + 0.000213569 r + 0.0000711895 $

- DataPoints = 167

- NbrofIVs = 2

- Sum of Squares Equation: 5242.57 + 4434.37 = 9676.95

- SSR + SSE = SST, where SSR, SSE, and SST are the sums of squares for

- predicted y’s

- residuals

- observed y’s

- Standard Error of the Regression = 5.19989

- = √(SSE / (Datapoints – (NbrofIVs + 1)))

- R-Squared = 0.541759

- Adjusted R-Squared = 0.536171

- AICc = 1029.82

Linear Regression on GDP, IMF, and Gini

- Regression Equation; y = 73.3606 – 12.435 g – 38.764 m + 0.00011775 $

- DataPoints = 167

- NbrofIVs = 3

- Sum of Squares Equation: 6057.69 + 3619.26 = 9676.95

- SSR + SSE = SST, where SSR, SSE, and SST are the sums of squares for

- predicted y’s

- residuals

- observed y’s

- Standard Error of the Regression = 4.71212

- = √(SSE / (Datapoints – (NbrofIVs + 1)))

- R-Squared = 0.625992

- Adjusted R-Squared = 0.619108

- AICc = 998.044

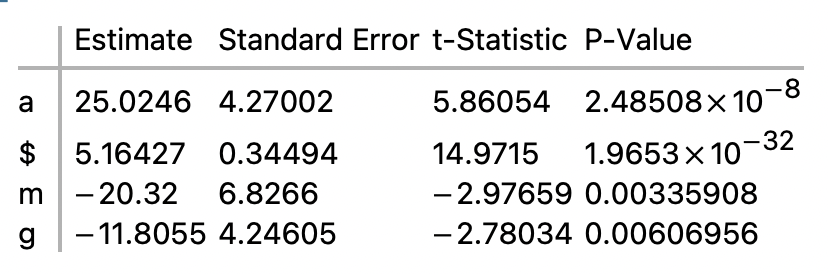

NonLinear Regression on GDP, IMF, and Gini

- Regression Equation; y = 25.0246 – 20.32 y – 11.8055 z + 5.16427 Log[x]

- DataPoints = 167

- NbrofIVs = 3

- Sum of Squares Equation: 6897.47 + 2779.48 = 9676.95

- SSR + SSE = SST, where SSR, SSE, and SST are the sums of squares for

- predicted y’s

- residuals

- observed y’s

- Standard Error of the Regression = 4.12941

- = Sqrt(SSE / (Datapoints – (NbrofIVs + 1)))

- R-Squared = 0.712773

- Adjusted R-Squared = 0.707487

- AICc = 953.955

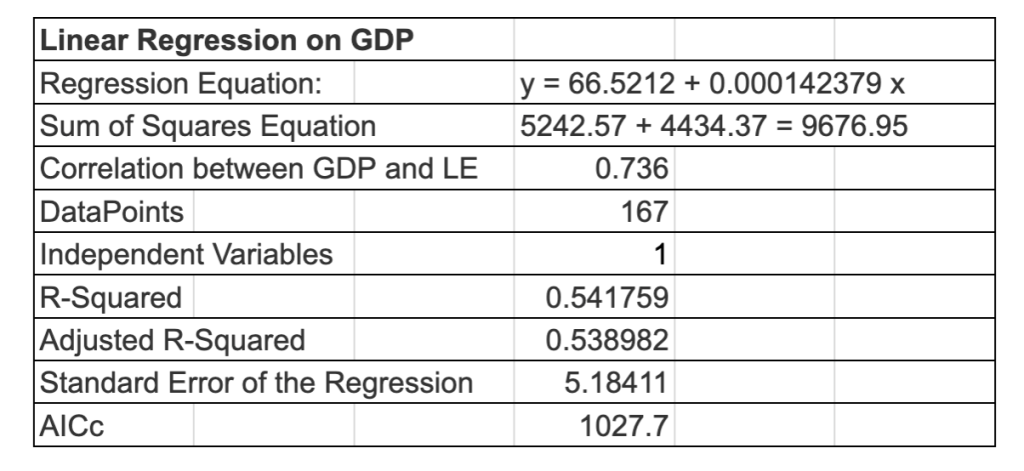

Linear Regression on GDP

- Linear Regression on GDP

- Regression Equation: y = 66.5212 + 0.000142379 x

- DataPoints = 167 and Independent Variables = 1

- Correlation between GDP and LE = 0.736

- Sum of Squares Equation: 5242.57 + 4434.37 = 9676.95

- R-Squared = 0.541759 and Adjusted R-Squared = 0.538982

- Standard Error of the Regression = 5.18411

- AICc = 1027.7

- Analysis

- Correlation

- Pretty good correlation between GDP and Life Expectancy, 0.736

- Graphs

- The data curves to the right, suggesting that a nonlinear regression might do better.

- Standard Error of the Regression

- We’ll see how 5.18411 compares to later regression.

- P-Values for t-Statistics for the standard errors of the coefficients

- Very high. But that’s assuming that the regression equation is correct.

- R-Squared and Adjusted R-Squared

- R-Squared is 0.541759, meaning that the regression captures about 54% of the life expectancy scatter. That’s fine, but not great.

- AICc

- We’ll see how 1027.7 compares to later regression.

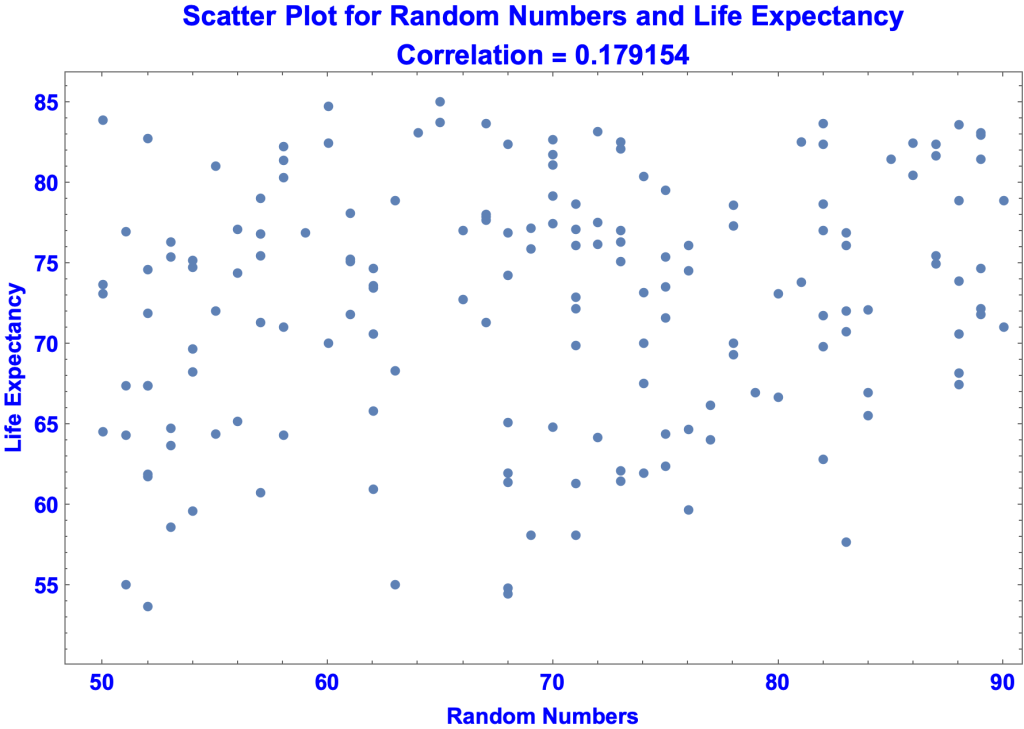

Linear Regression on Random Numbers

- Analysis

- Correlation

- Graphs

- Standard Error of the Regression

- P-Values for the t-Statistics for the standard errors of the coefficients

- R-Squared and Adjusted R-Squared

- 0.032096 versus SSE / SST = 0.967904

- AICc

Linear Regression on

- I’ll evaluate the regressions using

- Graphs

- Correlations

- The following metrics

- Standard Error of the Regression

- t-Statistics for the standard errors of the coefficients

- R-Squared

- Adjusted R-Squared

- AICc